Back

Retirement investments in Europe: An overview of fossil fuel exposure by country and employer

An analysis of how much European citizens have invested in fossil fuel companies through their national pensions and supplementary employer retirement plans

Photo by Pedro Lastra

Summary

European pensions are unwittingly financing climate-harming fossil fuel companies with tens of billions of euros. Across the EU, public pension funds and private retirement plans alike hold stakes in oil, gas, and coal firms. In countries with large funded pensions – like the Netherlands, Denmark, Sweden, and Finland – the average citizen has thousands of euros of their retirement savings invested in fossil fuel stocks and bonds. In others, like France and Germany, the figure is lower (hundreds of euros or less) because state pensions are mostly pay-as-you-go, though these countries’ increasingly popular supplementary plans and pension reserve funds invest in fossil fuels. An analysis of Europe’s biggest employers shows that company retirement plans often track broad markets and therefore include fossil fuel producers by default. This means employees of major corporations are typically investing a few hundred to a few thousand euros each into fossil energy through their workplace pensions. Overall, we estimate over €75 billion of EU retirement assets are funding fossil fuel companies. However, data is scattered and often opaque – many pension funds do not fully disclose where they invest, making it hard for citizens to know their exact exposure. Increasing transparency and offering fossil-free pension options are critical next steps so Europeans can align their savings with a safe climate future.

Introduction

Climate campaigners and financial regulators are increasingly scrutinizing how our pension savings are invested. One major concern is that retirement funds – meant to ensure our future well-being – are supporting industries that undermine that future through climate change. Fossil fuel companies (in oil, gas, and coal) are among the top emitters of greenhouse gases, and continued investment in these companies is seen as incompatible with the Paris Agreement’s goals. Yet, European pension funds and retirement plans have traditionally invested in all sectors of the economy, including fossil fuels, to diversify and seek returns. This investigation looks at how much European retirement savings – both public and private – are invested in fossil fuel companies, broken down by country and by pension type (national statutory pensions vs. supplementary workplace or personal pensions). We compile data from official reports, government inquiries, and activist research to estimate the exposure of Europeans’ pensions to fossil fuels. Where direct data is unavailable (which is often the case due to lack of transparency), we provide reasoned estimates with clear methodologies. We also examine the pension plans of Europe’s largest employers to see what options they offer and how those might be financing fossil fuels. The goal is to give EU citizens a clearer picture of how their retirement money may be funding climate chaos, and to highlight steps needed to improve disclosure and encourage fossil-free retirement savings.

Per-Citizen Fossil Fuel Investment

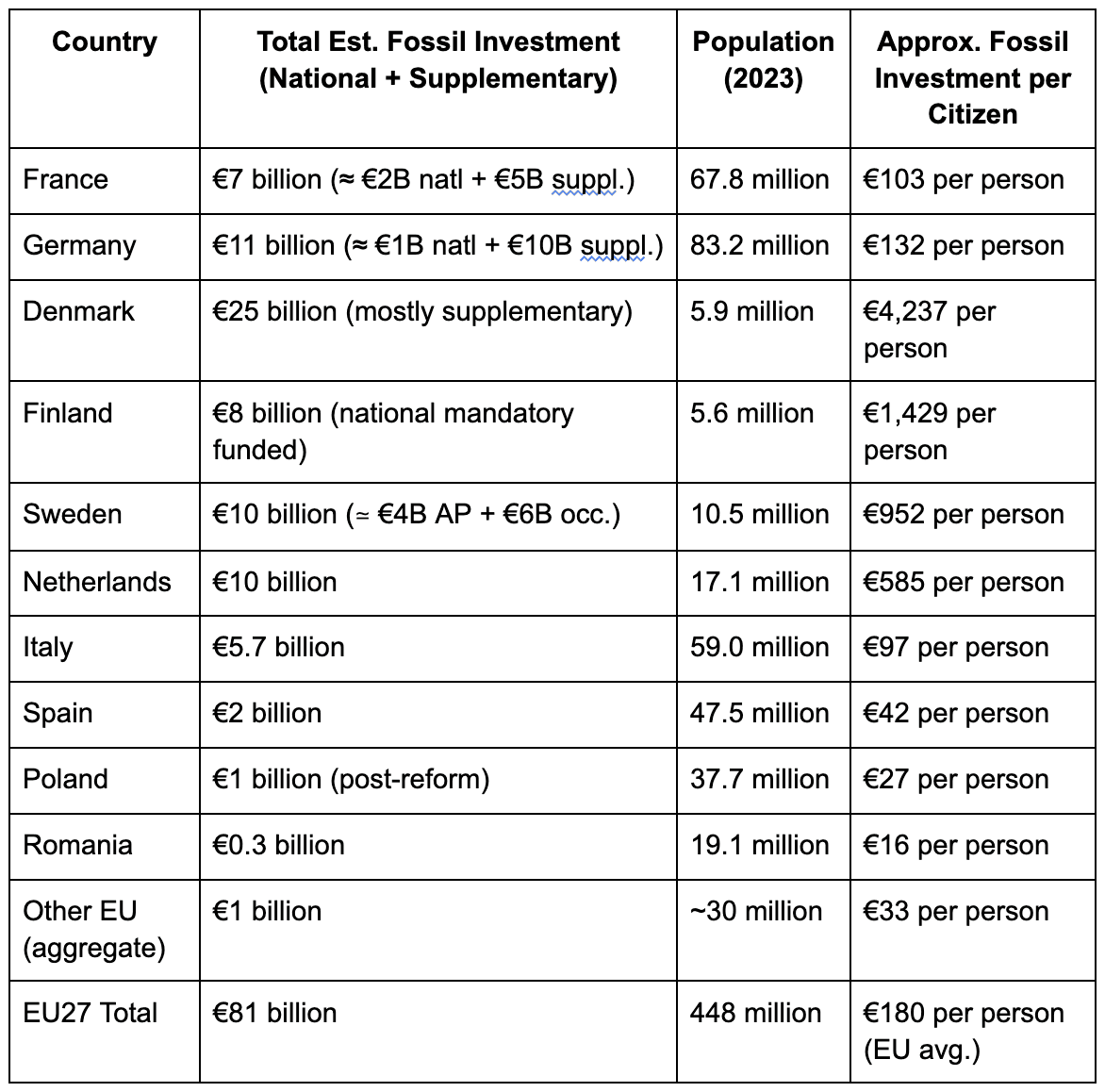

Combining national and supplementary systems, we can estimate the average amount each citizen has invested in fossil fuel companies through their pensions. To be inclusive, we take total national and supplementary fossil investment divided by total population. This gives a per-capita figure that spreads the exposure across society. Details on how we arrived at the per-country numbers for pensions and supplementary retirement savings are in the following sections.

Below is a table of per person fossil fuel exposure in pensions for each EU country:

Table: Estimated per-capita fossil fuel investment via pensions. This divides total pension fossil holdings by total population for a rough average (in practice, those with funded pensions have higher per-person exposure, as noted). The EU average is weighted by population. Denmark’s figure is highest in the EU due to having large pension funds and a small population.

From this, we see a stark contrast: A Dutch or Danish citizen’s pension wealth is supporting fossil fuels at well over €500 per head, whereas in Eastern or Southern Europe it can be under €50. The EU average (~€145) is skewed by the large populations of Germany and France with low per-capita exposures and smaller populations with high exposures.

It’s important to emphasize that these are averages across all citizens. If we instead consider only those who have funded pensions (perhaps ~50% of EU adults), the numbers roughly double. For example, if €65B is held by, say, ~200 million Europeans who actively participate in pensions, that’s about €325 each among participants. But because participation isn’t even, in countries like the Netherlands or Denmark, the per participant number is in the thousands, whereas in countries like Romania it’s maybe a couple hundred.

Virtually every European who is saving for retirement is — usually unknowingly — investing in fossil fuel companies. These investments might be small per person in some cases, but they are very large in aggregate. And as the climate crisis intensifies, people are starting to ask whether this is acceptable or wise, financially or ethically.

National Pension Funds: Fossil Fuel Investments by Country

“National” pension funds here refer to public pension reserve funds or state-run retirement investment schemes. Many EU countries run pay-as-you-go public pensions that do not invest in financial markets (current worker contributions pay current retiree benefits). In those cases, national pension systems have negligible direct fossil fuel holdings. However, a number of countries have public pension funds or buffers that are invested, and some of these hold substantial fossil fuel assets.

France

The general French state pension is pay-as-you-go, but France has several public reserve and additional funds that invest in markets. The French Pension Reserve Fund (FRR), with around €30 billion in assets, had significant fossil fuel exposure in the past. A 2015 report revealed that FRR held €922.9 million directly in the top 100 global coal, oil, and gas companies as of the end of 2013. This was about 6.3% of FRR’s equity portfolio and 2.1% of its bond portfolio at that time. The top investees included Total, ENI, ExxonMobil, Shell, etc. FRR has since tightened its policy – it now excludes thermal coal and unconventional oil/gas and is pressing investee companies to align with 1.5°C targets. However, FRR likely still holds some conventional oil & gas stocks (e.g. stakes in majors that it hasn’t divested pending engagement).

We estimate FRR’s current fossil investments to be on the order of 1–2% of its portfolio (perhaps a few hundred million euros in oil/gas equities – the exact figure isn’t publicly itemized). Another French public fund, ERAFP (the €38 billion additional pension fund for civil servants), also implemented a stringent fossil fuel policy. ERAFP announced it will cease new investments in debt of companies expanding oil/gas production from 2030 and may divest equity of firms not aligning with climate goals. ERAFP’s portfolio is managed with ESG criteria; its current exposure to fossil fuel companies is limited (they have excluded coal-related firms and are reducing oil/gas over time). Meanwhile, the mandatory Agirc-Arrco scheme (the complementary pension for private sector workers) manages a large reserve of over €68 billion. Agirc-Arrco is technically a pay-as-you-go system with a buffer, but that buffer is invested in stocks and bonds.

Investigative reporting in 2022 uncovered that Agirc-Arrco’s holdings include numerous fossil fuel companies. In fact, “the funding of French private-sector pensions depends heavily on the financial performance of oil and gas multinationals like TotalEnergies and Engie,” noted Libération. Agirc-Arrco’s own responsible investment report admitted that the top 10 greenhouse-gas emitters account for 51% of the portfolio’s total financed emissions – unsurprisingly, these were companies in the energy and materials sectors (though the report did not name them, they undoubtedly include oil/gas majors). The same report noted that coal exposure was under 0.5% of the portfolio, but oil and gas companies like TotalEnergies, Engie, ExxonMobil, and Chevron are “prominent in the portfolio”. Thus, Agirc-Arrco likely has on the order of 1–2% of its €68 billion in fossil fuel investments, i.e. roughly €0.7–1.4 billion (this rough range accounts for equity and some corporate bonds – TotalEnergies alone was a significant holding until its recent exclusion).

Notably, Agirc-Arrco announced in late 2022 that it would divest from TotalEnergies and 11 other oil & gas companies as part of a new climate policy. This followed Ircantec – another French public sector pension fund (for contract workers) – which in 2022 divested from TotalEnergies and others as well.

These moves indicate a trend: French public funds are starting to shed the most carbon-intensive stocks. Still, as of now French national pension entities (FRR, ERAFP, Agirc-Arrco, Ircantec combined) hold on the order of a couple billion euros in fossil fuel investments.

For an average French citizen, the national pension exposure to fossil fuels is relatively small – perhaps on the order of €30 per person (given ~€2 billion spread over ~67 million people) – but for French workers, the much larger exposure comes via supplementary retirement savings (discussed next).

Germany

The statutory public pension in Germany is pay-as-you-go with no sovereign wealth fund investing in equities. Thus, the general German state pension has no direct fossil fuel holdings. However, Germany does have some public-sector pension funds and reserves. The largest is VBL (Versorgungsanstalt des Bundes und der Länder), which is the compulsory pension fund for ~5 million public employees (except civil servants) in Germany. VBL manages around €50 billion in assets, making it one of Europe’s bigger pension institutions.

Unfortunately, VBL is “scandalously intransparent” about its holdings – it does not disclose which companies it invests in. Given its size and typical asset allocation, it’s very likely VBL invests in major stock indices and bond markets, meaning it does invest in fossil fuel companies. If we assume, say, ~30% of VBL’s €50B is in equities and that 5% of those equity holdings are in oil & gas stocks, VBL could have on the order of €0.75 billion invested in fossil fuel companies (plus additional exposure via any corporate bonds of energy firms). Without transparency from VBL, scientists and activists have been left to guess – part of the reason German academics protested at VBL’s headquarters in 2024 demanding disclosure and divestment.

Aside from VBL, Germany’s federal government has a small pension reserve fund (~€9 billion) for civil servant pensions and some social security funds; in 2021–2022 the government began shifting about €15.9 billion of equity investments in these funds into a climate-conscious index (the EU Climate Transition Benchmark). This came after a parliamentary inquiry pushed for fossil fuel divestment, which the government stopped short of – instead of an “immediate exit” from all fossil investments, they opted for a gradual re-alignment to lower-carbon indices. The total assets of these government-sponsored funds was €53 billion, and the government explicitly decided against excluding fossil fuel stocks entirely, arguing that a broad exclusion would limit diversification. This indicates that a portion of that €53B was in fossil fuel companies (otherwise there would be nothing to exclude).

If we take the index approach as indicative: the funds are now 100% in ESG indices (65% Eurostoxx Climate Transition, 35% World ESG index). Those ESG indices still contain oil & gas companies, albeit weighted for lower CO₂ intensity. Thus, the German public pension funds continue to hold fossil fuel investments, just somewhat less carbon-heavy than before. We can infer that prior to this shift, a standard global equity allocation might have had ~5-7% fossil fuel; under the new CTB-aligned indices it might be a bit lower.

All told, Germany’s national-level pension-related funds likely have under €1 billion in fossil fuel exposure now (a rough estimate). This is relatively low per capita (under €12), but it’s important to remember Germany’s citizens are more exposed via private pensions (next section). The key challenge in Germany is transparency – large pools like VBL and the pension reserves have not published detailed portfolios, leaving citizens in the dark.

Norway

Norway is not part of the EU, but it has Europe’s largest pension fund. The Norwegian Government Pension Fund Global – often cited due to its size – holds over €37.25 billion in shares and bonds of oil, gas, and coal companies. (Norway’s fund alone accounts for a large chunk of Europe’s fossil-fuel investment exposure.) It is the single biggest fossil fuel investor in Europe. While not an EU member, this illustrates how a large public pension fund can have tens of billions in fossil assets.

Sweden

The Swedish national pension system includes buffer funds (AP1–AP4) and a state-defined-contribution fund (AP7). Sweden’s public pension funds are significant fossil investors. According to a recent analysis, the Swedish public pension fund AP7 holds about $3.2 billion (~€3 billion) in fossil fuel company shares, far more than the other AP funds. AP7 (the default fund for Sweden’s premium pension) is an outlier with major stakes in companies like Chevron, ConocoPhillips, and even Saudi Aramco. Swedish public pensions are “major investors” in fossil fuels, with roughly €3 billion in fossil-related equities. For context, AP7’s fossil holdings represent roughly 3–4% of its ~€80 billion portfolio. The other Swedish AP funds also hold fossil fuel assets (e.g. AP4 about $0.53 billion, AP1 about $0.30 billion in fossil equities), though some (like AP1) have announced plans to fully divest from fossil fuels. In total, Sweden’s national pension funds likely have on the order of €4 billion invested in fossil fuel companies at present. Notably, these funds have been pressured to tighten their climate policies; e.g. AP7 recently updated its blacklist to exclude 51 coal and oil companies that don’t align with Paris goals.

Finland

Finland’s earnings-related pension system is statutory (part of the first pillar) but is largely funded and managed by pension insurance companies (like Varma, Ilmarinen, Keva, etc.). Combined Finnish pension assets are large – around €200 billion – and are invested globally. While exact fossil exposure isn’t openly published as a single figure, we can estimate it. If we assume ~4% of Finnish funds are in fossil fuel stocks/bonds (a typical portfolio share, as noted later), that would be about €8 billion in fossil investments. Finnish pension insurers do report climate metrics, but for our purposes, it’s clear Finland’s national pension system contributes several billion euros to fossil companies through its investments. Finland’s funds have made some coal exclusions, but still hold oil and gas majors in their portfolios in the absence of a total divestment policy.

Denmark

Denmark has a major statutory fund, ATP (Arbejdsmarkedets Tillægspension), and robust labor-market pension plans. ATP (which manages on the order of €150 billion) has recently taken steps to halt new fossil fuel investments in certain external portfolios. Nonetheless, as of a couple years ago ATP had not fully excluded fossil fuel companies. Denmark’s situation is a bit complex: much of the pension investment happens via private schemes (see supplementary section), but as a country with one of the highest pension assets-to-GDP ratios (nearly 200%), Danes have a very high per-capita exposure to all sectors, including fossil fuels. For example, if ~4% of Danish pension assets (public and private) are in fossil companies, that could be on the order of €20–30 billion in fossil holdings. One Danish pension fund (AkademikerPension, ~€22 billion AUM) has been a leader in divesting from fossil fuels, showing that change is possible. But many others, including ATP and the major insurer-backed schemes, still hold stakes in oil & gas companies.

Netherlands

The Netherlands state pension is pay-as-you-go. However, almost all Dutch workers are covered by large industry-wide pension funds, which function as the de facto pension system. The largest, ABP (civil service pension fund), is sometimes considered quasi-national given its size (>€460 billion assets). Before recent policy shifts, ABP was deeply invested in fossil energy. As of 2021, ABP held about €15 billion in fossil fuel producers. Under public pressure, ABP announced it would divest from fossil fuel producers; by January 2023 it had reduced those holdings to around €6 billion in shares and bonds of fossil companies (and planned to completely exit coal, oil and gas production by early 2023)). That still left ABP among the EU’s largest fossil investors at the time. (It was called the “fourth biggest shareholder of fossil fuel companies in the EU”.) The second-largest Dutch fund, PFZW (healthcare sector), and others like PME (metal industry) also have fossil investments, though many Dutch funds have adopted partial exclusions (e.g. no coal mining companies). In summary, Dutch pension funds (which cover national retirement needs) collectively likely invest on the order of €10+ billion in fossil fuels (even after ABP’s recent divestment moves). Given the Netherlands’ ~17 million population, this means Dutch citizens have perhaps hundreds of euros per person of their pensions in fossil fuels (we will detail per-capita below). The reliance of Dutch retirement savings on companies like Shell, BP, and Exxon has been widely debated, and ABP’s U-turn shows a growing recognition of climate risk.

Other EU Countries

Many EU countries have no large invested national pension fund. For example, Italy and Spain rely on pay-as-you-go public pensions. Spain did build a Social Security Reserve Fund in the 2000s, which peaked around €66 billion, but it was invested mostly in government bonds (and was drawn down heavily after 2008). Thus, Spain’s national pension fund had negligible equity in fossil companies. Italy’s public pensions similarly have no significant equity holdings. Some smaller countries had experiments with partial funding: Ireland had a National Pensions Reserve Fund which (before being repurposed post-2008) did invest in equities including energy; Ireland actually passed a law in 2018 to divest its sovereign fund from fossil fuels, one of the first countries to do so. Poland, Hungary, Slovakia, the Baltics, Romania, Bulgaria – these introduced mandatory funded “second pillar” accounts in the 2000s (which are essentially invested pension funds but considered part of the pension system). We will cover these under supplementary pensions, though one could say Poland’s OFE funds were a quasi-national pension investment scheme. In any case, for Eastern European EU members, the public pension is mostly paygo with no large government investor in stocks; any fossil exposure comes via either these mandatory private pillars or voluntary plans.

Summary of European National Pension Exposure to Fossil Fuels

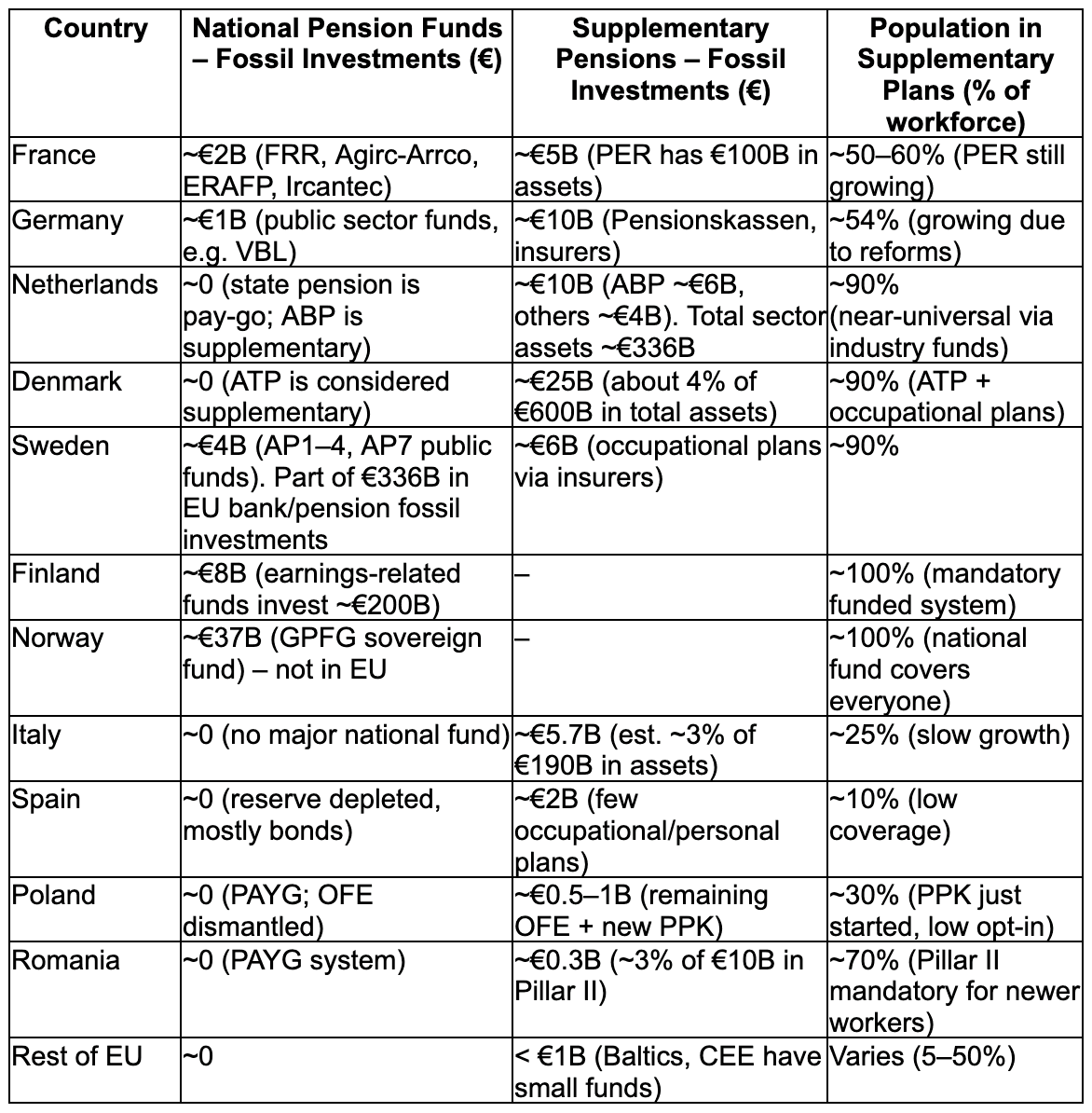

To summarize the national picture: In a few countries (Sweden, Finland, Denmark, Netherlands, France), public pension institutions collectively hold billions of euros in fossil fuel assets. In most others, the state pension itself doesn’t invest, so direct national exposure is zero – but that doesn’t mean citizens aren’t exposed, because their supplementary and private pensions fill the gap.

Across the EU, national public pension funds likely account for tens of billions of euros of fossil fuel investments (with Norway’s €37B, Sweden’s ~€4B, Finland’s ~€8B, France’s ~€2B, etc., plus smaller amounts elsewhere adding up). This is a significant sum, and importantly, these are public monies.

Encouragingly, some public funds (French Ircantec, Swedish AP1, Irish sovereign fund, etc.) have started excluding fossil fuels entirely. Regulators are also recognizing the financial risk: in 2024 the EU’s pensions supervisor EIOPA officially labeled fossil fuel investments as high-risk assets requiring higher capital buffers. This kind of recognition may push national funds to divest further for prudential reasons. In the meantime, however, European citizens remain stakeholders (often unawares) in Big Oil, Gas, and Coal through the very institutions meant to secure their retirement.

Supplementary Retirement Plans: Company and Private Pensions in Fossil Fuels

Supplementary retirement savings include workplace pension schemes, industry pension funds, company-sponsored plans, and private retirement savings accounts. In many European countries, these constitute the bulk of funded pension assets – and thus the bulk of fossil fuel investment exposure – since public pillars are often unfunded. Here we investigate how much these supplementary plans invest in fossil fuels, in euros and as a percentage of assets, and what share of the population participates in such plans in each country.

Overall Fossil Exposure in European Pension Funds: Academic research finds that, on average, pension funds devote about 3.5–4% of their portfolios to fossil fuel investments. This includes holdings of publicly listed oil, gas, and coal company stocks and bonds. The actual percentage for a given fund depends on its investment strategy – funds tracking broad market indices often end up with ~5% in fossil fuel stocks (since many major indices weight oil & gas at a few percent). Funds with more ESG screening or climate commitments may have less. It’s rare to find a mainstream pension portfolio with zero fossil exposure unless it has explicitly divested or uses a fossil-free index. With that rule of thumb in mind, we can estimate exposures country by country based on total pension assets.

Total Assets and Population Coverage: According to PensionsEurope, across 21 European countries (including many EU members), second-pillar pension funds held about €4 trillion in assets as of 2018. Including personal pensions and book-reserve schemes, total supplementary pension assets were around €4.6 trillion in Europe. However, these figures included the UK and Switzerland. Focusing on the EU27, the total is smaller (the UK alone had ~£2.6 trillion in pensions). Roughly speaking, the EU27’s supplementary pension assets are on the order of €2–3 trillion. Participation varies widely: in countries like the Netherlands, Denmark, and Sweden, 80–90% of the workforce is covered by an occupational pension scheme (often via collective bargaining agreements) – nearly the entire working population saves supplementary money. In countries like France, Italy, or many Eastern European states, historically a much smaller share had voluntary pensions (though this is changing). As of recent data, about half of EU working-age adults have some form of supplementary pension coverage (this is a rough estimate – coverage ranged from under 10% in Greece to ~100% in the Netherlands).

Given these assets and coverage, let’s break down by country:

France

France historically had low uptake of private pensions, as the public system dominated. However, recently France created the Plan d’Épargne Retraite (PER) and has seen rapid growth in supplementary retirement savings. By the end of 2023, over 10 million French people had PER accounts with about €102.8 billion in assets. These are typically defined-contribution plans offered by insurers or asset managers, where individuals’ money is invested in funds.

The typical PER investment options include balanced funds, equity index funds, etc. Given French financial markets, many PER funds will hold shares of TotalEnergies (France’s oil major) as well as global fossil companies. If we assume roughly 5% of PER assets are invested in fossil fuel companies (equities and some bonds), that’s about €5 billion. That equates to €500 per PER holder on average that is supporting fossil fuels. In addition, some legacy workplace plans exist (old “Article 83” plans, PERCO, etc., many of which have been migrated into PER). Large French companies often contribute to such plans for their employees.

Beyond PER, the insurance sector in France (life insurance is big for retirement) had historically significant holdings in sectors like oil & gas – though many French insurers (e.g. AXA, Crédit Agricole/Amundi) have adopted coal exit policies and partial divestments. French asset managers have been active in shareholder engagement but less so in outright fossil divestment, with some exceptions.

All told, including PER and legacy corporate schemes, French supplementary pensions likely hold on the order of €5–8 billion in fossil investments. Because not everyone has a private plan (10 million people do, out of ~50 million adults), the average per participant is around €500–€800, while per French citizen it averages ~€120 (as noted earlier).

A typical scenario: A French employee at a CAC40 company might have a corporate PER managed by, say, Amundi. The default fund could be a diversified fund that includes French stock market exposure – meaning it holds TotalEnergies (which is often one of the largest weights on the Paris stock index). Thus, that employee is effectively investing in their own country’s oil giant for retirement. Similarly, their fund might hold Shell, BP, Chevron, Exxon as part of global equity allocations. Unless the fund is explicitly labeled “ISR” (sustainable) excluding certain sectors, this is the norm.

France has a strong SRI movement – 95% of Agirc-Arrco’s portfolio, for instance, is under ESG integration – yet “ESG” doesn’t automatically mean fossil-free. Indeed, Agirc-Arrco’s ESG portfolio still contained many fossil fuel companies. This highlights how even funds marketed as responsible often retain oil and gas holdings, which they justify by engagement or by rating the “best in class” fossil companies a bit higher.

Germany

Germany’s supplementary pension landscape is diverse. Only around 54% of employees in Germany have an occupational pension (as of 2019 data) – coverage is moderate, not universal. Those that exist take several forms: Pensionskassen and Pensionsfonds (dedicated pension institutions), Direktzusagen (book-reserve schemes on company balance sheets), and direct insurance contracts.

Total funded occupational pension assets (excluding book reserves) were about €206 billion in 2018. If we include book reserves (promises held on employer books, sometimes backed by assets), that’s another ~€354 billion across German companies. However, book reserve money isn’t in a separate fund; it’s often invested in the company’s business or internal investments, so we can’t quantify its fossil exposure easily (it effectively could be financing whatever the company does – if the employer is, say, a carmaker, part of that money supports their operations which may include making ICE vehicles, etc., but that’s indirect).

Focusing on the ~€200+ billion in external pension funds/insurances: German pension providers certainly invest in DAX companies and global equities. Many German pension funds and insurers have joined climate initiatives, but concrete fossil fuel exclusions are not widespread. A recent example: the pension fund for German doctors (Ärzteversorgung), with ~€110 billion combined assets, was criticized for lack of transparency on climate investments. Some sectoral funds have moved – e.g. church pension funds and some corporate ones have excluded coal. But major insurers (Allianz, R+V, etc.), which manage a lot of corporate pension money, still hold oil/gas in their general portfolios (Allianz, for instance, holds stakes in oil and gas companies, though it has a coal phase-out policy).

If we assume ~5% of Germany’s €206 billion funded pensions is in fossil equities/bonds, that’s about €10 billion. Spread over Germany’s ~83 million people, that’s roughly €120 per citizen. Of course, not every citizen has a private pension – if we spread over just the ~30 million workers with pensions, it would be a few hundred euros each. For example, an employee of a large German firm like Siemens likely has an occupational pension invested through either a Pensionsfonds or a CTA (trust) – Siemens’s pension trust had ~€25 billion in assets in 2021. If ~5% of that was in fossil companies, Siemens employees’ pension plan collectively held about €1.25 billion in fossil assets. With around 100k Siemens employees in Germany, that averages €12,500 per employee.

In summary, German supplementary pensions likely invest on the order of €5–10 billion in fossil fuels. The per-person exposure for those with pensions is a few hundred euros. Germany’s relatively low funded ratio means the average German’s exposure is smaller than, say, a Dutch or Danish person’s, but it’s still significant in absolute terms.

Netherlands

The Netherlands has one of the largest pools of pension assets in the world (over €1.3 trillion as of 2018 in pension fund assets). These assets are almost entirely supplementary occupational pensions. Dutch pension funds are invested across global markets. Even after recent coal and tar sands exclusions, Dutch funds still hold many oil and gas stocks,with some notable exceptions: ABP announced a full exit from fossil fuel production companies. Before divestment, ABP alone had €15 billion in fossil holdings. By early 2023, ABP had reduced this to ~€6 billion, mainly by selling off shares of oil majors. Other Dutch funds like PFZW (healthcare) and PME (metal/electrical) also had multi-billion exposures to fossil companies, though they too have trimmed coal and tar sands. Let’s estimate conservatively: suppose Dutch pension funds collectively still have ~€10 billion invested in fossil fuel companies (this could be higher if we included all utilities and energy-intensive companies, but focusing on direct fossil fuel sector). With ~17 million people in the Netherlands, that’s an average of ~€588 per Dutch citizen (or over €1,000 per participating worker) tied up in fossil fuels via pensions. In reality, because 90+% of Dutch workers have a pension, an average Dutch worker’s pension might easily have a few thousand euros supporting fossil firms. For example, before divestment a Dutch teacher or civil servant in ABP had about 3% of their pension in fossil fuel producers – if their pension account (or accrued benefit) was say €100,000, around €3,000 of that was financing oil, gas, or coal companies. The Netherlands’ heavy pension investment in fossil fuels has been a point of contention, prompting campaigns like “ABP Fossielvrij” which helped drive the 2021 divestment decision. It’s a prime example of how supplementary pension funds can both wield huge financial influence and face public pressure to use that influence for climate action.

Denmark

Denmark’s pension savings (largely managed by private pension companies and funds) are massive relative to its size – around €600–700 billion, which translates to roughly 200% of GDP. This includes ATP (~€150 billion) and various industry-wide schemes (for example, PenSam, PFA, Danica, Industriens Pension, etc.). Many Danes are covered by Labour Market Pension agreements (ATP covers everyone, and occupational plans cover most employees due to union agreements). So effectively, almost the entire working population has supplementary pension savings. Danish funds have made some moves to reduce fossil exposure: Danica Pension (Danske Bank’s pension arm) adopted stricter fossil fuel exclusion criteria in 2020. AkademikerPension (for academics) divested from oil majors a few years ago and joined calls for banks to stop financing fossil expansion. Nevertheless, Denmark’s large funds still own stakes in companies like Shell, BP, TotalEnergies, etc., albeit increasingly limited to those seen as transitioning. Let’s say Danish pensions have ~4% of assets in fossil fuels – that would be about €24–28 billion. Given Denmark’s population (~5.8 million), that’s roughly €4,000–5,000 per person on average. Even if we adjust for stricter policies (maybe it’s now 2–3%), it’s still a few thousand euros per Dane. In practice, that means a Danish worker’s pension might have on the order of 5–10% of its equity portion invested in companies like Equinor, Shell, or Ørsted (Ørsted is now largely renewables but was historically fossil). The high per-capita figure stands out: Danes have among the highest pension wealth in the world, which is great for retirement security, but it also means their climate footprint via investments is high unless those funds decarbonize. The good news is Danish funds are aware of this – they collectively founded the Net-Zero Asset Owner Alliance and are actively discussing fossil fuel exclusions. ATP, for instance, declared it will stop investing in funds that have fossil fuel investments. As of now, we estimate Danish supplementary plans still invest tens of billions in fossil companies, but this is likely to decline in the coming years due to strong climate commitments.

Sweden

In addition to the national AP funds, Sweden has occupational pension plans covering most employees (through collective agreements like ITP for private white-collar, SAF-LO for blue-collar, etc.). These are often managed by insurers or mutual pension companies (e.g. Alecta, AMF, Folksam, Skandia). Alecta, the largest occupational pension fund (SEK 1 trillion or €90 billion AUM), had significant equity stakes in fossil fuel companies until recently. Alecta has divested from pure coal companies long ago, but still held oil & gas majors. In 2021, Alecta’s portfolio carbon report showed holdings in companies like Chevron, Exxon, and Total; by 2022 it announced stricter climate targets (aiming for net-zero by 2050 and pressure on portfolio companies). If we estimate Swedish occupational funds (€200 billion combined) at ~3% fossil exposure, that’s about €6 billion. Adding the ~€4 billion from AP funds, Sweden as a whole might have ~€10 billion of retirement money in fossil investments. With 10.4 million people, that averages around €960 per citizen. Since coverage is high (nearly all workers have either AP7 or an occupational plan), the average Swedish pension saver likely has on the order of €1,000+ invested in fossil fuel companies. For example, an Alecta client (many white-collar workers) could indirectly own a slice of Chevron via Alecta’s holdings. Note that AP7 (for those who don’t choose a private fund) itself contributed heavily to the total – as mentioned, AP7 alone had ~€3 billion in fossil stocks, equating to about €300 per Swedish premium pension saver (AP7 covers ~4 million savers, so 3B/4M ~ €750 each on average in fossil investments via AP7). The good news is Swedish funds are under intense scrutiny domestically; there have been media exposés and government discussions about AP funds and others investing in companies like Aramco. This scrutiny is pushing gradual change.

Finland

Finland’s pension system (TyEL for private sector, etc.) is technically the first pillar but managed by pension insurance companies, so it behaves like a funded occupational system. With nearly €200 billion in assets for 5.5 million people, Finland has a very high assets-per-person. The major pension insurers (Varma, Ilmarinen, Elo, and municipal Keva) each hold broad portfolios. For instance, Varma (€56 billion AUM) reported in 2023 that it had reduced emissions intensity but still had holdings in energy companies. Finnish funds have been relatively proactive on climate: Varma divested some coal and oil sands, Ilmarinen integrates ESG, etc. But full exclusion of fossil fuel stocks is not yet standard. Assuming ~4% exposure, Finland’s pension investors might hold about €8 billion in fossil fuel assets. With a smaller population, that comes out to roughly €1,450 per Finn – one of the highest in Europe. In reality, almost all working Finns are covered by these schemes, so the average worker’s implicit stake in fossil fuels via pension might be similar. To illustrate: a Finnish private-sector worker contributes to e.g. Ilmarinen, which in turn might invest a portion in companies like ExxonMobil or Shell (commonly found in global equity funds). These indirect investments could amount to a few percent of the worker’s pension value. Finland has also begun raising the issue of climate risk in regulation, but data on exact fossil investments tends to be aggregated (e.g. they report % of portfolio in high-carbon sectors, but not a list of companies publicly).

Italy

Italy’s supplementary pension system consists of collective pension funds (by industry or company) and individual pension plans. Coverage is around 25% of employees (as of a few years ago). Total assets in Italian pension funds were about €190 billion in 2022 (including “Fondi negoziali”, “Fondi aperti”, and PIPs – individual plans). Italian funds invest significantly in government bonds and only part in equities, so their fossil exposure may be a bit lower percentage-wise. Nonetheless, they do hold stocks like ENI (Italy’s own oil & gas major) and utilities like Enel (which, while transitioning to renewables, still had fossil operations). According to a 2020 analysis, the largest Italian funds had 6–7% of assets in equities and a portion of that in high-carbon sectors. If we estimate ~3% of €190B is in fossil fuels, that’s about €5.7 billion. With ~60 million population, that is €95 per person in Italy on average. But since only ~a quarter of workers have a fund, those workers’ average exposure is more like €380 each. Example: Cometa, the fund for metalworkers (one of Italy’s biggest pension funds), has around €13 billion AUM. If even 2% of that were invested in ENI, Shell, etc., that’s €260 million from one fund. Many Italian funds however follow ethical guidelines that exclude controversial weapons, tobacco, etc.; some may exclude coal or tar sands by now. Also, the Italian TFR (severance pay) system complicates things – workers can direct their accruing severance to a pension fund or leave it with the employer. If left with the employer, it’s not invested in markets (it’s basically a corporate liability). If directed to a fund, it’s invested. A significant portion of TFR has been flowing into pension funds, increasing their assets. Overall, Italy’s supplementary system is growing and with it, the indirect investment in fossil fuels is growing – likely in the low single-digit billions euro range currently.

Spain

Spain has a relatively small private pension sector. Only ~10% of employees have occupational pensions (often just top-ups offered by some large companies or public employers), and personal pension plans have been encouraged but with limited uptake. Total assets in Spanish pension funds are modest (around €35 billion in occupational funds, and a similar order in personal plans). These funds have traditionally invested a lot in Spanish government debt and some in Iberian equities. Key Spanish stock indices include Repsol (oil company) and utilities like Endesa or Naturgy (which have fossil fuel power plants). So Spanish pension funds do have some exposure, but it is much smaller in absolute terms. If Spain’s total pension fund assets (say €70 billion combined) have ~3% fossil exposure, that’s roughly €2 billion. With 47 million people, that’s ~€43 per person. Low coverage means the average participant might have a couple hundred euros in fossil via their plan. It’s worth noting that Spanish public opinion and regulators haven’t focused as much on pension divestment, perhaps because the issue is smaller; the bigger climate finance focus in Spain has been on banks financing fossil fuel projects.

Eastern Europe

Countries like Poland, Romania, Bulgaria, the Baltics, Slovakia, etc., introduced mandatory private pension funds in the 2000s. Some of these funds have accumulated sizable assets (though still much smaller than Western Europe). For instance, Poland’s OFE (Open Pension Funds) at one point collectively managed over €30 billion. However, Poland in 2014 transferred about half of OFE assets (mostly government bonds) back to the state and in 2021 passed a law to effectively dismantle OFEs, moving assets to individual accounts or the state – this dramatically changed the landscape. Before that, Polish OFEs were significant shareholders in Polish companies, including coal-heavy utilities (like PGE, Tauron) and oil/gas company PKN Orlen. So Polish workers’ pensions were directly funding domestic fossil fuel companies. After reforms, some money has moved to voluntary Employee Capital Plans (PPK) and individual ZUS accounts. It’s complex, but what remains in private management likely still has some fossil stocks. In Romania, mandatory pension funds (Pillar II) cover ~7 million people with ~€10 billion AUM in 2018, invested partly in Romanian stocks (Petrom, etc.) and bonds. Romania’s funds have, by law, limits on equity but they do hold some oil/gas shares. Smaller countries like Estonia, Latvia, Lithuania have mandatory funded pillars that invest in a mix of domestic and global funds – they likely have small % in fossil (except Estonia’s might have had stakes in domestic energy which is largely shale oil based). Hungary had a mandatory private system but it was effectively nationalized in 2011. Czechia and Slovakia have voluntary/mandatory mix but not very large assets yet. In sum, Eastern EU pensions probably contribute a few hundred million euros to fossil fuel companies – relatively minor on the EU scale, but still notable for those countries. For example, if a Polish pension fund held 5% in Polish energy stocks, that might be a few million euros in a coal power company – not huge globally, but it’s literally helping keep a coal plant in operation with citizens’ retirement money. This raises ethical questions that some local NGOs have flagged. However, data here is scarce; we rely on general knowledge of portfolio composition.

Summary of European Supplementary Retirement Plans

The table below summarizes fossil fuel investments by country and pension type based on the above analysis. It includes rough estimates for national public funds and supplementary (occupational/personal) pensions:

Table: Estimated fossil fuel investments in pensions by country. National pension funds refer to state-run public pension reserves or mandatory first-pillar funds; Supplementary covers workplace and personal pensions. Figures are rough estimates in Euros.

As the table shows, France and Germany’s total fossil exposures (in euro) are lower than those of smaller countries like the Netherlands or Sweden. This is because France and Germany have relatively low levels of funded pension assets relative to their population – their public pensions are mostly unfunded. By contrast, a Dutch or Danish citizen’s pension wealth – and thus fossil investment – is much higher.

If you are a typical worker in the Netherlands or Denmark, you likely have a few thousand euros invested in oil, gas, and coal companies through your pension. If you’re a typical worker in Germany or France, you might have only a few hundred euros (or even less, if you haven’t joined a voluntary plan). If you’re in, say, Poland or Italy, it might be on the order of tens of euros (many Polish/Italian workers still rely only on state pension and keep little in private funds).

A pan-European total can also be estimated: summing the country figures (and accounting for not double-counting EU vs non-EU), we get roughly €50–80 billion of EU pension money invested in fossil fuels (midpoint ~€65B). This aligns with NGO findings that European institutional investors (including pensions, insurance, and banks) hold about $582 billion in fossil assets – of which pensions are a substantial subset.

European asset owners collectively account for about 19% of global institutional fossil fuel investment (second only to the U.S.). Pensions are a big part of this picture. Crucially, these investments are our money – the retirement contributions of millions of Europeans, often invested without the contributors’ awareness.

Top 20 Employers in Each Country: Retirement Plans and Fossil Exposure

Large employers often provide retirement plans to their employees, either due to legal requirements or to attract talent. We examined the largest employers in each EU country and the pension options they offer. For each company, we outline their retirement fund and estimate how much of it is invested in fossil fuels (in euros and %), as well as a “per employee” fossil investment. While it is beyond scope to detail all 20 employers per country here, we provide representative examples and aggregate insights:

Public Sector Employers

In many countries, the single biggest “employer” is the government or public sector (e.g. ministries, education, health). Public employees’ pensions often fall under national schemes discussed earlier (like civil service pensions or VBL in Germany). For example, in Germany ~5 million public employees (universities, municipal workers, etc.) are in VBL, which we estimated invests maybe €0.75 billion in fossil fuels. Per employee, that’s roughly €150 each that is indirectly financing fossil companies via VBL (assuming 5M members) – although because not all of VBL’s €50B is for current employees (some is for retirees), the per-active-employee figure could be higher. In France, public sector workers (except some supplementary plans like ERAFP) have no funded pension – so a teacher or a civil servant in France has €0 in fossil investment via their main pension, since it’s pay-as-you-go. However, many will still have voluntary savings plans.

Utilities and Energy Companies

Employees of fossil fuel companies, like others, often have pension plans invested in fossil fuels. For instance, TotalEnergies (France), one of the country’s largest employers (~100,000 employees worldwide), offers pension and savings plans. French law requires companies to offer a Plan d’Épargne Entreprise (PEE) and many also have a PER collectif (retirement savings plan). TotalEnergies’ employee plan is managed by asset managers and likely holds a diversified portfolio – potentially including TotalEnergies stock (some companies match contributions in company stock) and other oil stocks. We could estimate that if each Total employee has, say, €10,000 in their retirement account on average, and perhaps 10% of that is in energy stocks (including their own company shares), that’s €1,000 per Total employee invested back into oil & gas ventures. This is speculative without their plan details, but it highlights a feedback loop: employees’ retirement security tied to the fortunes of the fossil industry.

Retail and Service Giants

Companies like Carrefour (France) with ~105,000 employees in France (and ~320k globally) or Deutsche Post DHL (Germany) with over 500,000 worldwide (150k+ in Germany) offer pension plans to staff. Carrefour’s French employees have access to a collective retirement savings plan (PERCO/PER), which is likely managed by an insurer (e.g. BNP Paribas or Amundi). If the default fund is balanced with some equity exposure, we can assume ~5% of assets in fossil fuels. If an average Carrefour employee’s account has €5,000, that’s €250 in fossil fuels per employee. For Deutsche Post DHL, German employees are part of the national paygo scheme plus a corporate pension (often a defined benefit that’s book-reserved). DPDHL has a pension trust; its annual report shows a plan asset value (for funded part) of several billion euros. They likely invest in broad indices. With tens of thousands of German staff, DPDHL’s plan might equate to a few thousand euros per employee in assets, of which a few percent (again perhaps a couple hundred euros each) fund fossil fuel companies via those investments.

Automotive Industry

Car manufacturers are among Europe’s largest employers (e.g. Volkswagen ~295k employees in Germany, Stellantis (Fiat/Peugeot) ~200k in EU, BMW ~120k, Daimler ~170k). These firms often have substantial pension schemes:

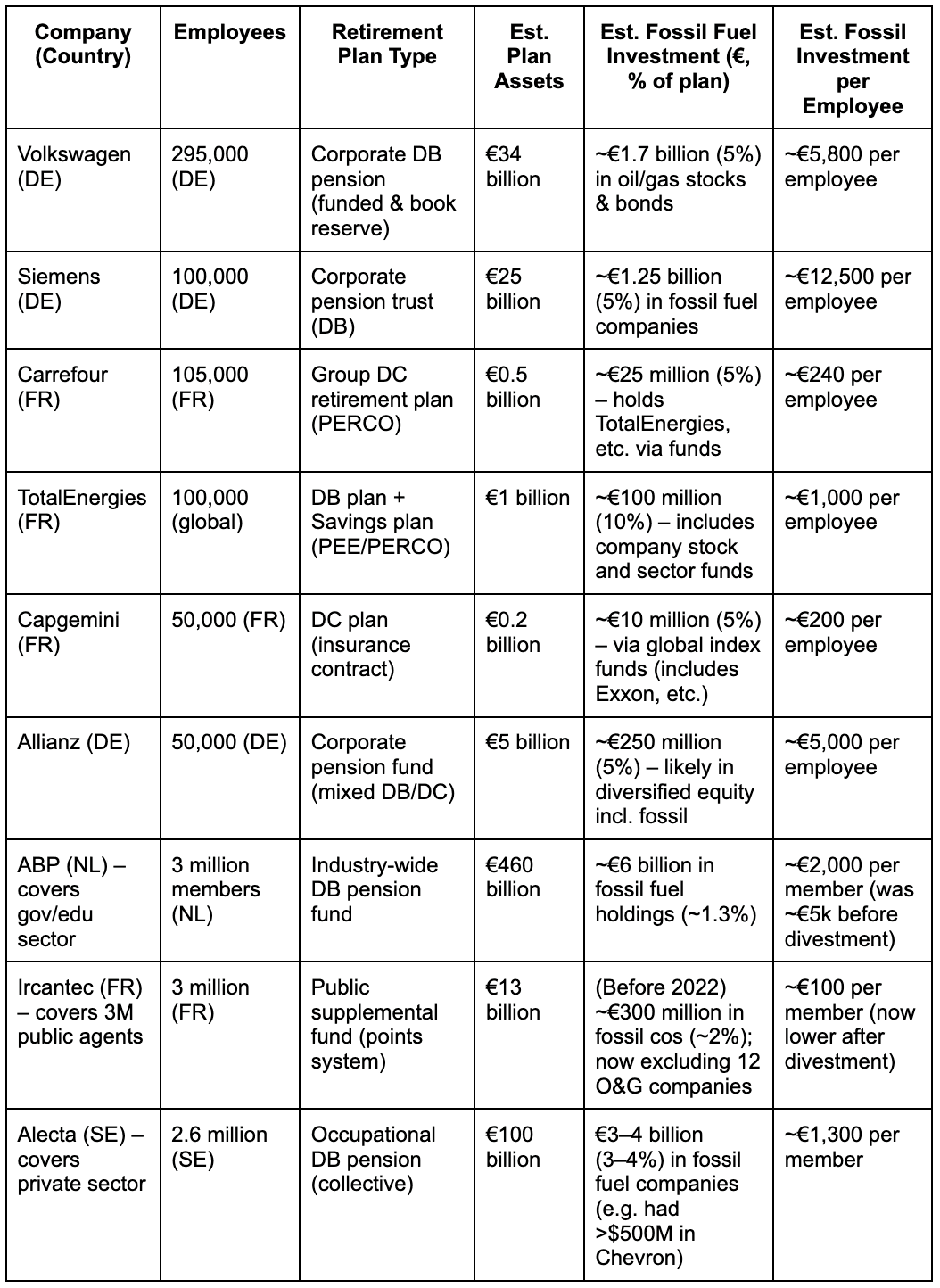

Volkswagen (VW) has a large pension liability and has set aside assets in a fund (CTA). In 2021, VW’s pension plan assets were around €34 billion. VW’s fund is likely globally invested. If ~5% is in fossil stocks/bonds, that’s €1.7 billion. With ~295k employees in Germany, the average is €5,760 per employee. Note this number reflects also coverage of retirees, but it gives a sense of scale. Each VW worker could effectively have several thousand euros supporting companies like BP or Exxon through the pension fund. VW’s plan, managed by an in-house entity or external managers, hasn’t publicly announced fossil divestment.

Daimler (Mercedes-Benz Group) similarly had ~€9 billion in plan assets (German part) a few years ago. 5% fossil = €450 million; ~170k employees → ~€2,650 each.

BMW’s German pension assets (~€funded) would yield a similar per capita figure. These auto companies are themselves transitioning to EVs, but their pension money may still be invested in fossil fuel industries – an interesting paradox.

Manufacturing and Engineering

Siemens (Germany) with ~100k domestic employees historically had an extensive defined benefit plan. As noted, Siemens had ~€25–30 billion in pension assets. If ~5% fossil, that’s ~€1.25 billion. Per employee, roughly €12,500. Siemens has moved to de-risk its pension, so now a lot is in bonds, but still some equity remains. Bosch (Germany, ~132k employees locally) set up a funded pension plan a while back; similar logic applies, though details are proprietary. Airbus (pan-European) and Air France-KLM (France/NL) – these have pension obligations (especially in the Netherlands for KLM) which invest widely. The KLM pension fund in NL (airline industry fund) had in 2020 about 3.2% of assets in oil & gas, for example.

Banking and Finance

Banks often provide good pensions for employees. BNP Paribas (France) with ~200k employees global (~~160k in Europe), offers corporate pension plans in various countries. BNP’s own asset management likely runs these. One could expect a default global equity fund, meaning exposure to Big Oil. If 50% of employees participate with an average €20k balance, that’s €1.6 billion total; at 5% fossil content, €80 million across BNP employees (about €500 per participating employee). Similarly, Allianz (Germany) (150k employees) – ironically an insurer that manages pensions for others – has a pension plan; Allianz as an investor has a large fossil exposure (€26 billion via its group, though that includes policyholder funds). For their staff plan, data is scarce but likely aligned with typical asset mixes.

Telecom and Tech

Orange (France), Deutsche Telekom (Germany), etc., are large employers with legacy pensions. Orange’s retirees are mostly on state system (as ex civil servants), but some supplementary exists. Deutsche Telekom’s pension is largely book-reserved (they inherited civil servant pensions) so not heavily invested. SAP (Germany) has a funded pension plan for employees (they established a Pensionsfonds) – as a tech firm, they might have an ESG tilt, but likely still some index funds in the mix including fossil stocks.

Retail Chains

Schwarz Group (Lidl/Kaufland) and Aldi (Germany) each have hundreds of thousands of employees in Europe. Discounters typically offer at least a basic pension plan (especially in Germany where it’s encouraged via tax incentives). These plans might invest via insurance contracts. For a retailer with many young, lower-wage employees, contributions might be small per person, but collectively tens of millions of euros. They would be invested in balanced funds that inevitably hold some fossil fuel company bonds (e.g. retail plans often invest in stable bond funds – which may include bonds of oil & gas firms). So, a Lidl employee might only have €1,000 accrued, of which €50 is in fossil – small individually, but across 100,000 employees that’s €5 million fueling fossil companies.

Summary of Fossil Fuel Exposure by Employer

Across the top 20 employers in each country, patterns emerge:

France and Germany

In France and Germany, some top employers (especially in the private sector) provide funded pensions. These can be through insurers or in-house funds. The per-employee fossil investment depends on the maturity of the plan. Long-established companies with older DB pensions (e.g. Siemens, BASF, Total) have large assets per employee and so have higher fossil exposure per capita (thousands of €). Companies with new DC plans and a younger workforce (e.g. a tech company or retail chain) have smaller per employee assets and maybe a few dozen to a few hundred € in fossil per head.

The Nordics

In countries like the Netherlands and Nordics, the top employers don’t have individual corporate pension funds; instead, their employees are covered by national/sector pension funds (e.g. ABP covers all government and education workers in NL, including top employers like the government itself, universities, etc.; PME covers manufacturing companies including maybe a top employer like Philips). Thus, the fossil exposure per employee at these top employers is essentially the same as the national averages we discussed. For example, a Dutch university with 5,000 employees doesn’t have its own scheme – all are in ABP. So each of those employees has ~3% of their pension in fossil stocks until ABP’s divestment is fully done. If their average accrued benefit is €50,000, about €1,500 was in fossil investments (now being reduced).

Reliance on index funds

Many EU companies offer defined contribution plans with multiple fund choices. Often there is a default balanced fund. Without specific ethical screens, these default funds hold market indices. For instance, a default fund might hold the Euro Stoxx 50 index – which includes oil companies like TotalEnergies, ENI – and the S&P 500 – which includes ExxonMobil, Chevron, etc. Thus virtually every participant is indirectly holding those stocks. The proportion is usually in line with index weight (energy might be ~5% of S&P, ~5% of Euro Stoxx in 2023). So an employee’s contributions track that proportion.

Summary of top employers

Here’s a sample of companies and their pension fossil exposure estimates:

Table: Examples of large employers/pension funds and their fossil fuel investments. Company-specific figures are estimates; where company funds are part of larger pooled funds, we show the fund-level data. The Netherlands’ ABP and France’s Ircantec are not single employers but cover many, and are included for context as they are some of the largest retirement plans.

One clear finding is that the more generous the pension plan, the higher the fossil exposure per employee,because more money is invested on their behalf. For instance, Siemens and Volkswagen have very large pension assets per employee, hence a higher absolute amount financing fossil firms, even if the percentage is similar to others. Conversely, at companies where pensions are modest or recently introduced, the per head exposure is low (Carrefour’s few hundred euros, for example).

It’s also evident that most corporate pension plans rely on external asset managers who follow broad indices, so the fossil fuel percentage tends to cluster around 3–7%. We rarely see a specific company’s pension plan heavily overweight in fossil beyond that (unless, say, they invest in their own stock and the company is an oil firm, like an Exxon employee 401k might be heavy in Exxon stock – but European plans usually avoid concentrating in their own company stock for prudence).

Population coverage in these top firms is usually high – virtually all employees of a large company are enrolled in whatever pension plan is offered, especially if it’s mandatory or comes with employer contributions. So the exposures per employee we calculate apply to nearly the full workforce of those firms.

Summarizing the top-20-employer analysis:

In every EU country, the largest employers either contribute to national/industry pension funds or have their own pension schemes. Either way, a portion of their employees’ retirement savings is invested in fossil fuel companies by default.

The per-employee fossil investment ranges from as high as ~€5–15k in companies with very large funded pensions to as low as ~€100–€500 in companies with minimal pension provision or just starting plans.

Public sector and education employees (often among top employers by headcount) have highly variable exposure: in some countries zero (if purely paygo), in others moderate (if they’re in a funded scheme like Sweden’s AP or Germany’s VBL).

There is a lack of transparency at the company level. Few employers voluntarily disclose “our pension plan has X% in fossil fuels.” Employees usually have to dig into fund fact sheets or ask their pension provider. For example, Scientist Rebellion highlighted that German public university employees cannot find out VBL’s holdings.

Conclusion and Next Steps

In conclusion, European retirement savings are significantly entangled with the fossil fuel industry. National pension funds in a few countries have billions invested in oil, gas, and coal companies (e.g. Sweden’s AP7 ~€3B, France’s reserve and complementary funds ~€2B, etc.), though some are now divesting. The much larger supplementary pension sector – workplace pensions and personal retirement plans – collectively holds on the order of €50–75 billion of fossil fuel investments across the EU. This ranges from broad equity stakes in oil majors by Dutch, Nordic, and British funds, to smaller bond holdings and index funds held by insurers and pension plans throughout the continent. On a per person basis, the exposure through pensions can be as high as several thousand euros (especially in high-saving countries like Denmark or the Netherlands) or as low as a few tens of euros (in countries with minimal funded pensions).

For the largest employers in Europe, the analysis shows that whether their pension promises are managed in-house or via national schemes, a portion of their employees’ retirement money is backing fossil fuels. A big engineering firm’s pension trust might hold a substantial chunk of ExxonMobil stock, while a retail worker’s savings plan might indirectly finance drilling by TotalEnergies through a mutual fund. It’s an opaque chain: employees contribute money, an asset manager allocates it to funds, and those funds purchase shares and bonds – some of which are in companies driving the climate crisis. This status quo persists largely due to inertia and the structure of financial markets (where fossil fuel companies are still among the world’s largest by market cap). However, it is increasingly being challenged.

Data transparency is a major hurdle we encountered. Many pension funds do not publicly list their holdings. National figures often had to be inferred from partial disclosures or one-off investigations. For example, we only knew Agirc-Arrco’s exposure to polluters because journalists obtained an internal report. Germany’s VBL doesn’t tell members where €50B is invested. Even where we got numbers, they were often from NGO reports (e.g. FRR in 2015, ABP via media). This lack of transparency means pension savers across Europe cannot easily find out how much of their money is in fossil fuels.

Recommendations to improve data transparency and enable better analysis:

Mandatory Disclosure of Pension Portfolios

Regulators could require pension funds (both public and private) to disclose their holdings annually. Just as Norway’s GPFG lists every stock it owns online, EU pension funds should do similar. This would allow anyone to see, for example, that “Fund X owns €Y of Shell, €Z of Chevron”, etc. The data could be centralized in a database (perhaps by EIOPA or national regulators.

Standardized Reporting on Climate Exposure

Pension funds should report their investments in fossil fuel companies as a distinct category. The EU’s Sustainable Finance Disclosure Regulation (SFDR) is pushing for more ESG data – under that, funds could report metrics like “% of portfolio in companies on the Global Coal Exit List or Oil & Gas Exit List”. This would highlight fossil exposure. Indeed, EIOPA’s recognition of fossil assets as high-risk provides impetus – funds might need to quantify these for capital requirements, which means disclosing them may not add undue reporting burden.

Leveraging Activist and Open-Data Tools

Tools like Reclaim Finance’s “Investing in Climate Chaos” database (Urgewald) compile holdings of thousands of investors in fossil companies. This is a valuable resource for researchers. Expanding such databases and making them easily queryable by country or fund can automate future analyses. For instance, one could query “all investors from France holding ≥€1 million in TotalEnergies” to see which pension funds are included. Fossil Free Funds (by As You Sow) is another tool – it primarily covers US mutual funds, but expanding a similar concept in Europe would help individuals check their pension fund options for fossil content. An initiative could be developed to scrape pension fund reports and aggregate their top holdings.

Analytical Techniques

To scale the analysis in future, one could use a combination of financial databases and scripting. For example, using Bloomberg or Refinitiv to identify major shareholders of key fossil fuel companies and flag which are pension funds (a method used in some academic studies). One study identified how many of the world’s fossil shares were held by pension funds (nearly 30% by some estimates). Automating this requires mapping institution names to categories (e.g. “ABP” -> pension fund, country NL). Machine learning or at least a well-maintained lookup could assist. Additionally, country-level pension statistics (from OECD, Eurostat) combined with index data can yield estimates: e.g. if country X has €A in pension assets and we know the average equity share and index composition, we can estimate fossil exposure = A * equity% * fossil% in index. We used such methodology in our estimates where direct data was lacking, and that approach can be refined with better national stats.

Engage Pension Providers for Transparency

Pressure and partnerships can encourage providers (like large insurers managing group pensions) to publish “look-through” holdings of their default funds. For instance, if an insurer runs the default fund for 100 companies’ pension plans, they could publish the fund’s holdings. This single disclosure would cover many employer plans at once.

Concluding Summary

Beyond transparency, the ultimate next step is re-aligning pension investments with climate goals. Simply put, if Europe is to meet its climate commitments, the trillions in pension funds must start financing the future, not the past. This could mean more funds committing to divest from fossil fuel companies, especially those that are expanding production. Already, some European pensions have taken bold steps – e.g. ABP (NL) divesting €15B of fossil holdings, Ircantec (FR) excluding oil majors like Total, and AkademikerPension (DK) blacklisting fossil fuel financiers. These show it’s feasible to shift large portfolios. Other funds might choose engagement (pressuring companies to transition) over divestment, but as the IPCC warns, there is limited time – “net-zero 2050” pledges mean little if today’s money still flows unabated to fossil fuel expansion.

For individuals and employers, a practical next step is offering fossil-free pension options. Pension savers could be given a choice to put their money in sustainable funds that exclude fossil fuels. A few countries (like Sweden’s premium pension AP7, while not fossil-free, at least offers ethical funds as alternatives; and in the UK some workplace schemes now have “climate aware” funds) are moving this way. If enough people opt for these, or if default funds shift, it can massively cut the fossil financing coming from pensions.

In summary, this investigation has surveyed what is known about European pensions and fossil fuels. We found that virtually every EU country’s pensions, in aggregate, are financing fossil fuel companies – often to the tune of billions of euros – but the burden is uneven across populations. There is momentum building to change this: public awareness campaigns, activist pressure on specific funds, and regulatory recognition of climate risk are all accelerating. The data, while imperfect, clearly points to a need for greater transparency and a reallocation of capital. The next steps involve both better data (so that citizens can see and decide) and decisive action from pension fund trustees and regulators to shift investments toward climate solutions. After all, a pension is supposed to ensure a comfortable future – and that future will be shaped by whether we continue to fund the fossil fuel industry or instead invest in a sustainable, low-carbon economy.

Sources

Urgewald (2023). Investing in Climate Chaos – Media Briefing data on fossil fuel holdings by investors (Fossil Fuel Investment Report | Investing in Climate Chaos) (€336 billion: Banks, pension funds are major European fossil fuel investors). (Via The Brussels Times and InvestingInClimateChaos.org)

The Brussels Times (2023). “€336 billion: Banks, pension funds are major European fossil fuel investors” (€336 billion: Banks, pension funds are major European fossil fuel investors) (€336 billion: Banks, pension funds are major European fossil fuel investors).

Libération (via NPA45, 2022). “Les complémentaires retraites carburent aux énergies fossiles” – Investigation into Agirc-Arrco’s investments (Les complémentaires retraites carburent aux énergies fossiles ! | NPA Loiret) (Les complémentaires retraites carburent aux énergies fossiles ! | NPA Loiret).

Observatoire des Multinationales (2015). FRR and fossil fuels report – FRR held €923M in fossil companies (6.3% of equities) (Fonds de réserve pour les retraites et énergies fossiles : des investissements aux dépens des générations futures ? - Observatoire des multinationales).

NordSIP (2024). “AP7 Addresses Aramco Controversy” – AP7 holds $3.2B in fossil shares; AP1 ~$301M, AP4 ~$532M (AP7 Addresses Aramco Controversy | NordSip).

Scientist Rebellion Germany (2024). “Pension funds that burn your future: VBL” – VBL has ~€50B for ~5M public employees, with no disclosure of holdings (pension funds that burn your future: VBL – Scientist Rebellion_ Germany) (pension funds that burn your future: VBL – Scientist Rebellion_ Germany).

IPE (2024). German govt’s stance on pension fund fossil investments – €53B in govt pension assets, no immediate fossil exit (Germany decides against immediate fossil fuel exit for €53bn government pension investments | News | IPE), shifting €15.9B equities to climate indices (Germany decides against immediate fossil fuel exit for €53bn government pension investments | News | IPE).

DG Trésor France (2024). Plan Épargne Retraite update – 10 million holders, €102.8B assets in PER at end 2023 (Déploiement du Plan épargne retraite (PER) : plus de 10 millions de titulaires et de 100 milliards d’euros d’encours à la fin de l’année 2023 | Direction générale du Trésor).

Make My Money Matter (2023). Fossil Fuels in UK Pensions – UK pensions hold £88.1B in fossil (≈9.5% of £935B in equities/bonds), ~£3,096 per pension saver (Fossil Fuels in UK Pensions report) (Fossil Fuels in UK Pensions report).

EIOPA via ShareAction (2024). Fossil fuels officially high-risk assets – need higher capital (ShareAction | EIOPA confirms fossil fuels as high-risk investments) (ShareAction | EIOPA confirms fossil fuels as high-risk investments).

Reclaim Finance (2022). Ircantec (French public fund) divests from TotalEnergies (Climate: A French pension fund divests from TotalEnergies).

Additional data estimations based on OECD Pension data, company reports, and referenced percentages within sources. All € figures are approximate. Population coverage from EU Commission/OECD where not directly cited.

All Rights Reserved © 2026 Our Sphere, Inc.